Categories

Financing a Maui home purchasePublished May 15, 2026

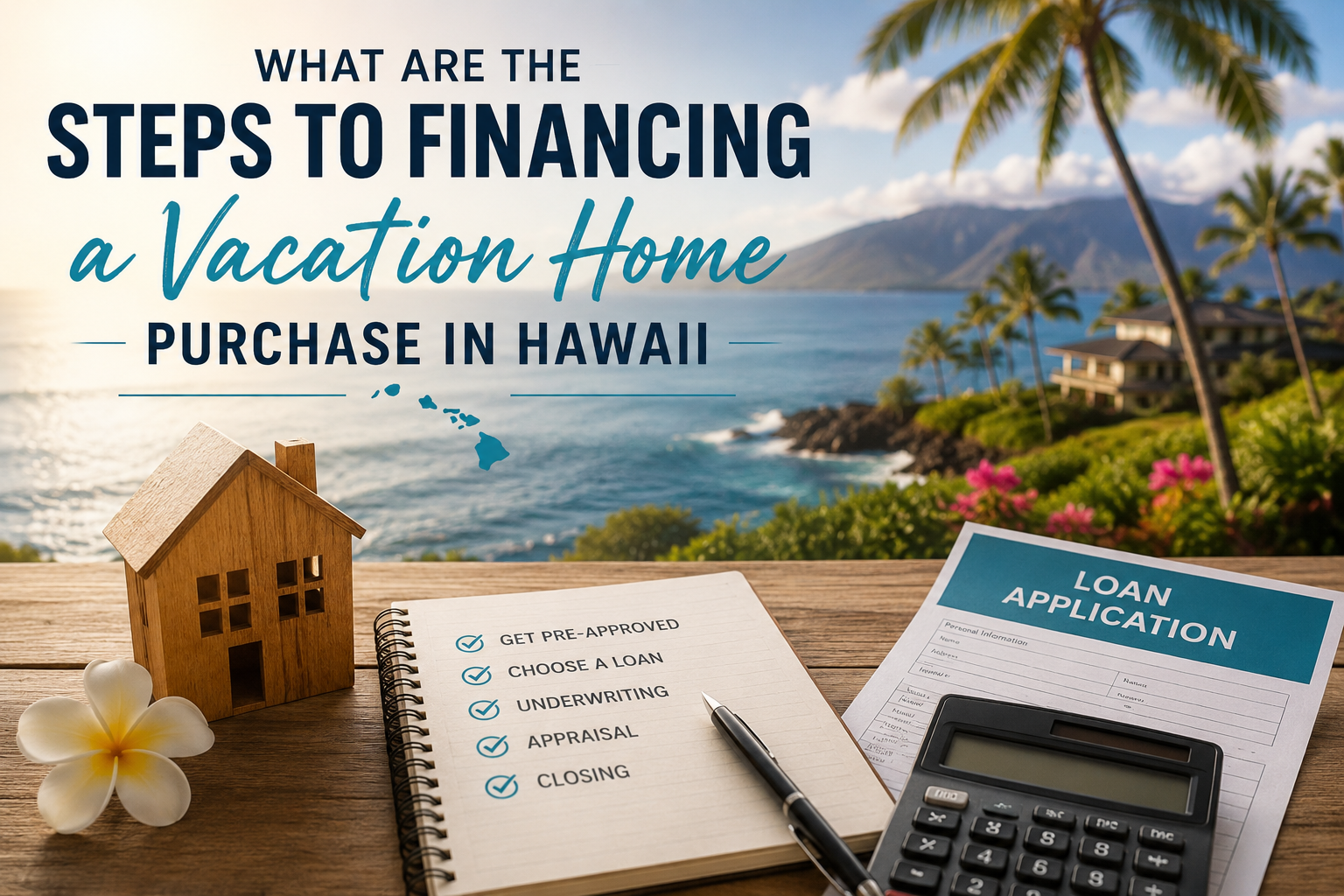

What Are the Steps to Financing a Vacation Home Purchase in Hawaii?

What Are the Steps to Financing a Vacation Home Purchase in Hawaii?

Buying a vacation home in Hawaii is exciting, but the financing process is usually more detailed than buying a primary residence. Lenders look closely at your income, debt, reserves, property use, insurance, HOA fees, and whether the home will be treated as a true second home or an investment property.

The basic steps are simple: get financially prepared, decide how you’ll use the property, get pre-approved, choose the right loan structure, write a strong offer, complete underwriting, and close with the right cash reserves in place.

Below is a clear step-by-step guide to financing a vacation home purchase in Hawaii.

Quick Answer: How Do You Finance a Vacation Home in Hawaii?

To finance a vacation home in Hawaii, you typically need to:

- Decide whether the property is a second home or investment property.

- Review your credit, income, debt, and cash reserves.

- Get pre-approved with a lender familiar with Hawaii real estate.

- Understand Hawaii’s conforming loan limits and jumbo loan options.

- Budget for down payment, closing costs, HOA fees, insurance, taxes, and reserves.

- Confirm whether rental income can be used to qualify.

- Make an offer with financing terms that match the property.

- Complete appraisal, underwriting, insurance review, and condo/HOA review.

- Review your Closing Disclosure at least three business days before closing.

- Fund the purchase and close.

For 2026, Fannie Mae lists the one-unit conforming loan limit for Hawaii at $1,249,125, which is higher than the baseline limit in most U.S. markets. Larger loans may require jumbo financing, depending on the property, county, and loan structure.

Step 1: Decide Whether the Property Is a Second Home or an Investment Property

Before you start looking at properties, you need to know how the lender will classify the home.

A second home is generally a property you occupy for part of the year, control exclusively, and do not treat primarily as a rental property. Fannie Mae’s second-home guidance says the property must be occupied by the borrower for some portion of the year, be suitable for year-round occupancy, and not be a rental property or timeshare arrangement.

An investment property is different. If your main purpose is rental income, especially short-term rental income, the lender may underwrite it as an investment property. That can affect your interest rate, down payment, reserve requirements, and documentation.

This matters a lot in Hawaii because many buyers want to use the property part-time and rent it part-time. That can be possible, but the loan type, zoning, HOA rules, county regulations, and rental history all need to line up.

Step 2: Review Your Full Financial Picture

Vacation home financing is usually more demanding than primary-residence financing. Lenders often look closely at:

- Credit score

- Debt-to-income ratio

- Down payment funds

- Cash reserves

- Existing mortgage obligations

- HOA or AOAO fees

- Property taxes

- Insurance costs

- Rental income, if applicable

- Number of financed properties you already own

If you already own a primary residence, the lender will usually count that mortgage, property taxes, insurance, and HOA fees in your debt ratio. If you own multiple properties, additional reserve requirements may apply, especially for second homes and investment properties. Fannie Mae notes that reserve requirements can apply based on the number of financed properties a borrower has.

For Hawaii buyers, reserves are especially important because many properties have higher carrying costs than mainland buyers expect.

Step 3: Choose a Hawaii-Savvy Lender

A Hawaii vacation home purchase is not the place to use a lender who rarely works with island properties.

A local or Hawaii-experienced lender can help you understand:

- Hawaii conforming loan limits

- Jumbo loan options

- Condo and condotel review issues

- Leasehold versus fee simple ownership

- Short-term rental restrictions

- AOAO documentation

- Insurance requirements

- Lava zones, flood zones, and coastal risk areas

- Appraisal challenges in low-inventory luxury markets

This is especially important for condos. Some Hawaii condos are easy to finance, while others may trigger more review because of litigation, insurance issues, high investor concentration, hotel-style operations, short-term rental use, or deferred maintenance.

Step 4: Get Pre-Approved Before Shopping Seriously

A pre-approval is different from a casual online estimate. A strong pre-approval usually means the lender has reviewed your credit, income, assets, debts, and purchase scenario.

For a Hawaii vacation home, the pre-approval should be specific to the type of property you want to buy. A pre-approval for a single-family home in Kihei may not automatically apply to a short-term-rentable condo in Kaanapali or a luxury property in Wailea.

Before making offers, ask your lender:

- What price range are you approved for?

- What down payment is required?

- Is the property being treated as a second home or investment property?

- Can rental income be used to qualify?

- Are you using conforming, jumbo, portfolio, or DSCR-style financing?

- How many months of reserves are required?

- Are there special condo review requirements?

- How quickly can the loan close?

A good pre-approval helps you avoid falling in love with a property that does not fit the financing.

Step 5: Understand Your Loan Options

Vacation home buyers in Hawaii commonly use several different loan types.

Conventional Second-Home Loan

This may work when the property is truly a second home and not primarily an income property. Second-home loans can have more favorable terms than investment loans, but the property use has to match lender guidelines.

Conventional Investment Property Loan

This may apply if the property will be rented out, especially if income is a major part of the ownership plan. Investment loans may require a larger down payment, stronger reserves, and different underwriting.

Jumbo Loan

Many Hawaii vacation homes exceed conforming loan limits. In that case, a jumbo loan may be needed. Jumbo loans often have stricter credit, reserve, and documentation standards.

Portfolio Loan

Some banks and credit unions keep loans in their own portfolio instead of selling them to Fannie Mae or Freddie Mac. This can sometimes help with unique Hawaii properties, higher-value homes, or condos that do not fit standard guidelines.

DSCR Loan

A debt-service coverage ratio loan may be considered by some investors when rental income is the main qualification factor. These loans are not the right fit for every buyer, and terms can vary widely, so they should be compared carefully.

Step 6: Budget for the Real Cost of Ownership

The purchase price is only one part of the budget.

For a Hawaii vacation home, buyers should also plan for:

- Down payment

- Closing costs

- Property taxes

- Homeowners insurance

- Hurricane insurance

- Flood insurance, if required

- HOA or AOAO fees

- Maintenance

- Utilities

- Property management

- General excise tax and transient accommodations tax, if renting legally

- Furnishings

- Repairs and capital improvements

- Reserves for vacancy or slower rental periods

This is especially important for resort condos and oceanfront properties. A condo with a lower purchase price may still have high monthly fees, insurance assessments, or upcoming building expenses.

Luxury single-family homes may have pool maintenance, landscaping, pest control, security, irrigation, solar, septic systems, private roads, or gate maintenance.

Step 7: Confirm Rental Rules Before You Rely on Rental Income

Many buyers ask whether they can use rental income to help qualify for a Hawaii vacation home loan. The answer depends on the property, the loan type, rental history, lease agreements, appraisal support, and lender guidelines.

Before relying on projected rental income, confirm:

- Is short-term rental use legal?

- Is the property in the correct zoning or approved use category?

- Does the HOA or AOAO allow vacation rentals?

- Is there rental history?

- Will the lender accept projected income?

- Is the property treated as a second home or investment property?

- Are taxes, licensing, and management costs included in the analysis?

This step is critical on Maui because short-term rental rules and proposed regulatory changes have created uncertainty in parts of the condo market. A property that looks strong on paper may not finance or operate the way a buyer expects.

Step 8: Write an Offer That Matches the Financing

Your offer should match the loan strategy.

For example, if the property is a condo, the offer timeline should allow enough time for lender condo review, document review, insurance review, and appraisal. If the property is high-end or unique, the appraisal may take longer because there may be fewer comparable sales.

A strong financing offer should account for:

- Loan type

- Down payment

- Appraisal timeline

- Condo document review

- Seller credits, if applicable

- Closing timeline

- Financing contingency

- Appraisal contingency

- Insurance availability

- Cash reserves after closing

In competitive luxury situations, sellers often look at the strength of the buyer’s financing, not just the offer price.

Step 9: Complete Appraisal, Underwriting, and Property Review

Once you are under contract, the lender will begin deeper underwriting.

This usually includes:

- Verifying income and assets

- Reviewing credit and debts

- Ordering the appraisal

- Reviewing title

- Confirming insurance

- Reviewing HOA or AOAO documents

- Checking flood zone or special hazard requirements

- Verifying funds to close

- Finalizing loan conditions

For condos, the lender may review the building’s insurance, budget, reserves, litigation status, owner-occupancy ratio, delinquency levels, and rental operations. This can be one of the most important steps in a Hawaii vacation home purchase.

Step 10: Review Your Closing Disclosure

Before closing, you will receive a Closing Disclosure showing your final loan terms, monthly payment, closing costs, and cash needed to close. The Consumer Financial Protection Bureau states that lenders are required to provide the Closing Disclosure at least three business days before the scheduled closing.

Review it carefully. Compare it with your original loan estimate and ask questions about anything that changed.

Pay close attention to:

- Interest rate

- Monthly payment

- Loan amount

- Cash to close

- Prepaid taxes and insurance

- Points or lender credits

- Escrow setup

- Closing costs

- HOA or AOAO prorations

Step 11: Fund the Loan and Close

The final step is wiring funds, signing closing documents, lender funding, and recording the deed.

In Hawaii, escrow and title handle many of the closing logistics. After recording, ownership officially transfers, and you can take possession according to the purchase contract.

Before closing, make sure you have a plan for:

- Utilities

- Insurance activation

- Property management

- Cleaning

- Furnishing

- Security

- HOA registration

- Rental onboarding, if applicable

- Local maintenance contacts

For off-island buyers, having a trusted local team matters. The purchase is only the beginning of vacation home ownership.

Common Mistakes to Avoid When Financing a Hawaii Vacation Home

The biggest mistake is assuming Hawaii financing works exactly like mainland financing. It often does not.

Other common mistakes include:

- Shopping before getting pre-approved

- Assuming every condo is financeable

- Relying on rental income before confirming lender rules

- Underestimating HOA fees and insurance

- Ignoring short-term rental regulations

- Confusing second-home and investment-property financing

- Forgetting reserve requirements

- Waiting too long to confirm insurance

- Making large financial changes before closing

- Choosing a lender unfamiliar with Hawaii properties

A well-structured financing plan can prevent delays, renegotiations, or failed escrow.

Final Thoughts: Financing a Hawaii Vacation Home Takes Planning

Financing a vacation home in Hawaii is absolutely possible, but it requires more preparation than a standard home purchase.

The most important steps are deciding how you will use the property, choosing the right lender, getting properly pre-approved, understanding the full cost of ownership, confirming rental and condo rules, and keeping the loan strategy aligned with the specific property.

On Maui, the details matter. A Wailea condo, a Kaanapali vacation rental, a Kapalua villa, a Kihei second home, and an Upcountry retreat may all require different financing conversations.

REALTOR® Benjamin Finnerty and The 808 Team help buyers evaluate Hawaii vacation homes from a practical, local perspective, including lifestyle fit, financing strategy, zoning, rental rules, HOA review, and long-term resale potential.

Schedule a free Hawaii vacation home consultation before you start writing offers.

Benjamin Finnerty REALTOR® RS-83812 · Keller Williams Realty Maui RB-21851

Call: 808-481-9748

Email: benjamin@the808team.com

Website: https://benjamin.the808team.com

The 808 Team Maui

| The 808 Team | Keller Williams Realty Maui

or another way