Categories

Financing a Maui home purchasePublished July 3, 2026

How to Finance a Maui Property in 2026: Conventional, DSCR, Bank Statement Loans, and Everything In Between

How to Finance a Maui Property in 2026: Conventional, DSCR, Bank Statement Loans, and Everything In Between

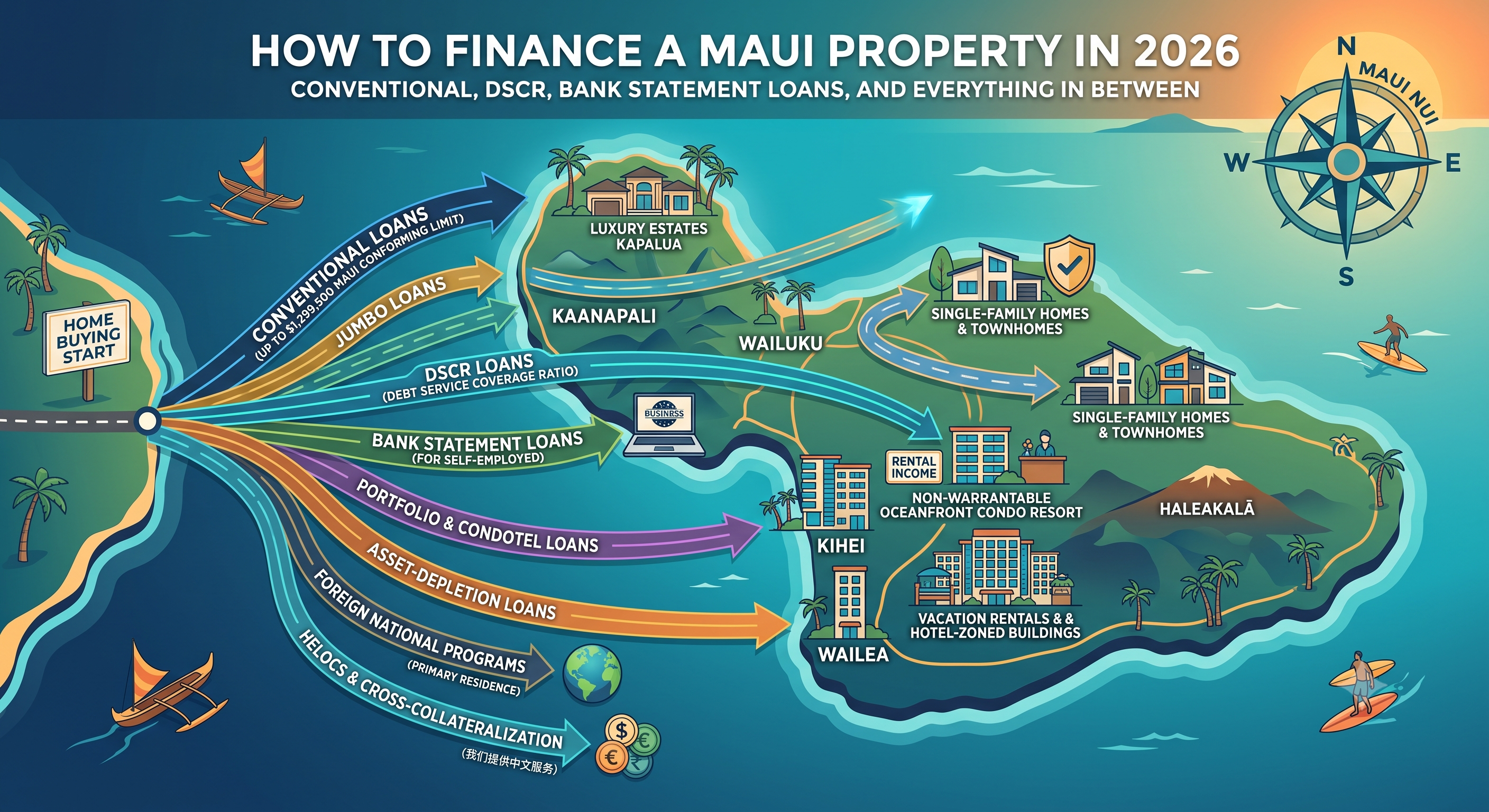

Quick Answer: Maui buyers in 2026 can finance property through conventional mortgages (up to Maui County's $1,299,500 conforming limit — the highest in Hawaii), jumbo loans, DSCR loans that qualify on rental income instead of personal income, bank statement loans for self-employed buyers, portfolio and condotel loans for non-warrantable buildings, asset-depletion loans, and foreign national programs. The right program depends less on you than on the property — many of Maui's best vacation rental condos don't qualify for conventional financing at all, which is why working with an agent who knows which lenders lend on which buildings matters.

If you've started shopping for property on Maui, you've probably discovered something frustrating: the loan your mainland lender pre-approved you for may not work on the condo you actually want to buy. That's not a Maui quirk — it's the defining feature of financing here. The good news is that the lending menu for Maui property is far bigger than most buyers realize. Let's walk through it.

Why Is Financing a Maui Property Different From the Mainland?

Two reasons: price point and property type.

On price, Maui is a high-cost market, but the federal government recognizes that. For 2026, Maui County's conforming loan limit is $1,299,500 for a single-family home — the highest in the state and among the highest in the nation. That means a buyer can borrow nearly $1.3 million and still get conventional, Fannie Mae-eligible pricing. On the mainland, that same loan would be a jumbo. This is one of Maui's best-kept financing advantages.

On property type, here's where it gets interesting. A huge share of Maui's most desirable investment inventory — oceanfront condos in Kihei, hotel-zoned resort condos in Wailea and Kaanapali, Minatoya List properties that carry legal short-term rental use — are what lenders call condotels or non-warrantable condos. These buildings have front desks, rental programs, short-term occupancy, or commercial elements that put them outside Fannie Mae and Freddie Mac guidelines. A conventional lender simply won't finance them, no matter how strong your credit is.

That's not a dead end. It just means you need a different door. Here are all of them.

What Loan Programs Can You Use to Buy Maui Property?

Conventional Mortgages: The Starting Point

For warrantable condos, single-family homes, and long-term rental properties, a conventional loan is usually the best pricing available. With Maui's $1,299,500 conforming limit, conventional financing covers a surprising amount of the market — including many townhomes and single-family homes in Kihei, Wailuku, and Upcountry. Second-home and investment-property conventional loans are available too, typically with 10% down for a second home and 15–25% down for an investment property.

The catch: the condo itself has to pass lender review. Owner-occupancy ratios, HOA budget reserves, insurance, litigation, and short-term rental activity in the building all get scrutinized. This is where deals die when buyers and agents don't check warrantability before writing the offer.

Jumbo Loans: For Maui's Luxury Tier

Above $1,299,500, you're in jumbo territory — which describes much of Wailea, Makena, and Kapalua. Jumbo loans typically require stronger credit (700+), larger down payments (often 20–30%), and more documented reserves. But competition among jumbo lenders is real, and portfolio jumbo programs can be surprisingly flexible on property type — some will even finance hotel-zoned condos that agency loans won't touch.

DSCR Loans: The Vacation Rental Investor's Workhorse

If you're buying a legal short-term rental on Maui, this is probably the program you'll use. A DSCR loan (Debt Service Coverage Ratio) qualifies the property, not you. The lender asks one question: does the rental income cover the mortgage payment? No tax returns, no W-2s, no debt-to-income calculation on your personal finances.

For Maui's STR-zoned and hotel-zoned condos — where gross rental income can be substantial — DSCR loans are often the cleanest path to closing. Typical terms: 20–25% down, credit score of 660+, and rates modestly higher than conventional. Many DSCR lenders will use short-term rental income projections (via market data or existing rental history), which matters enormously on Maui, where a condo's vacation rental income can be double what it would earn as a long-term rental.

DSCR lenders are also far more comfortable with condotels and non-warrantable buildings. For buyers targeting Minatoya List properties or resort-zoned inventory, DSCR is frequently the answer.

Bank Statement Loans: Built for the Self-Employed

Many Maui buyers are business owners, entrepreneurs, or 1099 earners whose tax returns — after legitimate write-offs — dramatically understate their real income. A bank statement loan solves this. Instead of tax returns, the lender qualifies you on 12–24 months of personal or business bank statement deposits.

If you run a business and your accountant does their job well, this program can be the difference between qualifying for a Kihei studio and qualifying for a Wailea two-bedroom. Expect 10–20% down and rates somewhat above conventional, with the trade-off being that your actual cash flow — not your taxable income — tells the story.

Portfolio and Condotel Loans: Local Knowledge Pays

Several Hawaii-based banks and credit unions keep loans on their own books rather than selling them to Fannie Mae. Because they set their own rules, these portfolio lenders will finance properties agency lenders won't — including true condotels with front desks and mandatory rental programs. Local portfolio lenders also understand Maui buildings by name; they've financed units in the same complexes for decades. On a non-warrantable building, a local portfolio loan is often the most competitive option on the table.

Asset-Depletion Loans: For Wealth Without W-2 Income

Retirees and high-net-worth buyers often have seven figures in investment accounts but little "income" on paper. Asset-depletion (or asset-utilization) programs convert your liquid assets into a qualifying income figure — typically dividing your eligible assets over the loan term. If your balance sheet is strong but your pay stubs are nonexistent, this is your program.

Foreign National Loans: Yes, Non-U.S. Buyers Can Finance Maui Property

Maui attracts buyers from around the world, and financing is available even without U.S. credit history, a Social Security number, or U.S. income. Foreign national loan programs typically require 25–35% down and price above conventional, and many pair naturally with DSCR structures for investment condos. As a Mandarin-speaking agent, I work with international buyers on exactly these transactions — the process is more document-intensive, but very achievable with the right lender lineup. (我们提供中文服务。)

VA and FHA Loans: For Primary Residences

If you're buying a home to live in, don't overlook government programs. VA loans offer eligible veterans zero-down financing with no loan limit for those with full entitlement — a powerful tool in a market like Maui. FHA loans allow lower credit scores and down payments as small as 3.5%, with 2026 limits in Maui reaching well over $1 million for a single-family home. Neither works for vacation rentals or investment condos, but for primary-residence buyers they can be game-changers.

HELOCs, Cross-Collateralization, and Cash-Out Refinancing

Plenty of Maui purchases are funded by equity somewhere else. A HELOC or cash-out refinance on a mainland home can produce the down payment — or the entire purchase price — for a Maui condo. Buying "cash" this way also strengthens your offer, and delayed financing rules let you place a mortgage on the property shortly after closing to replenish your reserves.

Seller Financing and Creative Structures

In a market with longer days-on-market in certain segments, seller financing has quietly returned to the conversation. An owner with substantial equity may carry a note at a negotiated rate, sometimes on properties that are difficult to finance conventionally. These deals require careful structuring, but they exist — and knowing when to propose one is part of the job.

How Do You Know Which Loan Fits Which Maui Property?

This is the real question, and it's why financing on Maui starts with the building, not the borrower. Before you fall in love with a unit, you need answers to: Is the building warrantable? Is it on the Minatoya List or in a hotel district? What does the AOAO budget and insurance picture look like? Does the complex have litigation or reserve issues that will spook a lender? Which lenders have recently closed loans in this exact building?

I track this building-by-building across South Maui and beyond, because a pre-approval letter is worthless if it's from a lender who can't close on the property you're offering on. Matching the right buyer, the right property, and the right loan program — that's where deals actually get done.

Frequently Asked Questions About Financing Maui Property

What is the conforming loan limit for Maui in 2026? $1,299,500 for a single-family home — the highest conforming limit in Hawaii. Loans above that amount are jumbo loans.

Can I get a conventional loan on a Maui vacation rental condo? Sometimes, but often not. Many of Maui's short-term-rental and hotel-zoned condos are non-warrantable, meaning Fannie Mae and Freddie Mac won't back them. DSCR, portfolio, and condotel loan programs are the usual alternatives.

What is a DSCR loan and why is it popular on Maui? A DSCR loan qualifies you based on the property's rental income rather than your personal income — no tax returns required. Because Maui's legal vacation rentals generate strong gross income, many STR condos qualify comfortably.

How much down payment do I need for a Maui investment condo? Plan on 20–25% for most DSCR and investor programs, 25–35% for foreign national loans, and as little as 10% for a second home on conventional financing if the building is warrantable.

Can foreign buyers finance property on Maui? Yes. Foreign national loan programs don't require U.S. credit or income history, typically with 25–35% down. I regularly assist international and Mandarin-speaking buyers through this process.

Do rising or falling interest rates matter more than the loan program? The program usually matters more on Maui. A great rate on a loan that can't close on a non-warrantable building is worth nothing. Secure the right program first; optimize the rate second.

Ready to Talk Financing Strategy for Your Maui Purchase?

Every one of these programs has a place, and I've seen each of them close deals on this island. The starting point is a conversation about what you want to buy and how you earn — from there, I'll connect you with lenders who actually close on Maui properties, including the buildings other lenders decline.

Benjamin Finnerty, REALTOR® Salesperson (RS-83812) The 808 Team | Keller Williams Realty Maui 380 Huku Li'i Place, Suite 201, Kīhei, HI 96753 📞 808-481-9748 📧 benjamin@the808team.com 🌐 benjamin.the808team.com

Fluent in English and Mandarin Chinese — 我们提供中文服务,欢迎联系。

This article is for informational purposes only and does not constitute lending or financial advice. Loan programs, limits, and terms change; consult a licensed mortgage professional for current guidelines.

The 808 Team Maui

| The 808 Team | Keller Williams Realty Maui

or another way